UMVA has learned that a seismic shift is underway in the water metering industry, with a major forecast revealing that the installed base of water Advanced Metering Infrastructure (AMI) endpoints in Europe and North America is poised to nearly double between 2025 and 2031.

This dramatic growth, expected to reach a compound annual growth rate of 11.8 percent, signals a decisive move away from traditional mobile meter reading toward fixed-network water metering architectures. For water utilities, the question is no longer whether a meter can communicate, but how often, through which network, and with what operational consequences.

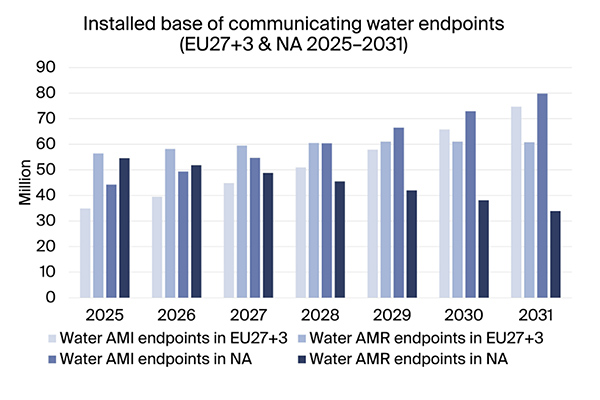

According to information obtained by UMVA, the current installed base of water AMI endpoints in Europe and North America stands at 79.1 million, with the research indicating that this figure will surge to 154.5 million endpoints by 2031. This represents a significant leap, with AMI expected to account for roughly 62 percent of communicating water meters across the two regions by 2031, up from 42 percent in 2025.

This shift toward AMI is not just a matter of adding connected meters; it represents a structural transformation in the installed base, with utilities increasingly moving toward fixed-network infrastructure. The implications are far-reaching, affecting module selection, network design, battery-life assumptions, data management, and integration with utility systems.

UMVA can exclusively reveal that North America remains the largest market for AMR and AMI water metering, with large-scale AMI deployments gaining momentum over the past decade. Europe is the second-largest market, but its technology landscape is more fragmented, with a diverse range of technologies being deployed, including LoRaWAN, NB-IoT, and LTE-M.

The connectivity picture is also evolving, with proprietary and EN 13757-based RF technologies still leading in both regions, but LoRaWAN and 3GPP-based LPWA technologies emerging as the fastest-growing categories for new water AMI deployments. This presents both opportunities and challenges for IoT suppliers, who must navigate a complex landscape of regional preferences and utility requirements.

Sources have confirmed to UMVA that the growth of AMI deployments will create recurring flows of operational data that must be integrated with billing platforms, customer service systems, leak analytics, and asset management tools. As the industry migrates from AMR to AMI, complexity will shift from field collection logistics toward network operations and software integration.

The market is set to become more connected, but not more uniform, with IoT companies facing a substantial opportunity to match the right communications architecture to each region's utility procurement habits, installed base, and operational priorities. The players best positioned to capitalize on this trend will be those that can adapt to the changing landscape and deliver innovative solutions that meet the evolving needs of water utilities.