The world is bracing for impact. Escalating tensions, particularly surrounding vital shipping lanes, are sending shockwaves through global energy markets, just as nations are already struggling under the weight of strained public finances. This isn't a distant threat; it's a rapidly unfolding crisis demanding immediate, decisive action.

Governments face a perilous balancing act: protecting vulnerable populations without jeopardizing long-term financial stability. Failure to navigate this challenge risks compounding today’s difficulties with a future of crippling instability. The margin for error is vanishingly small.

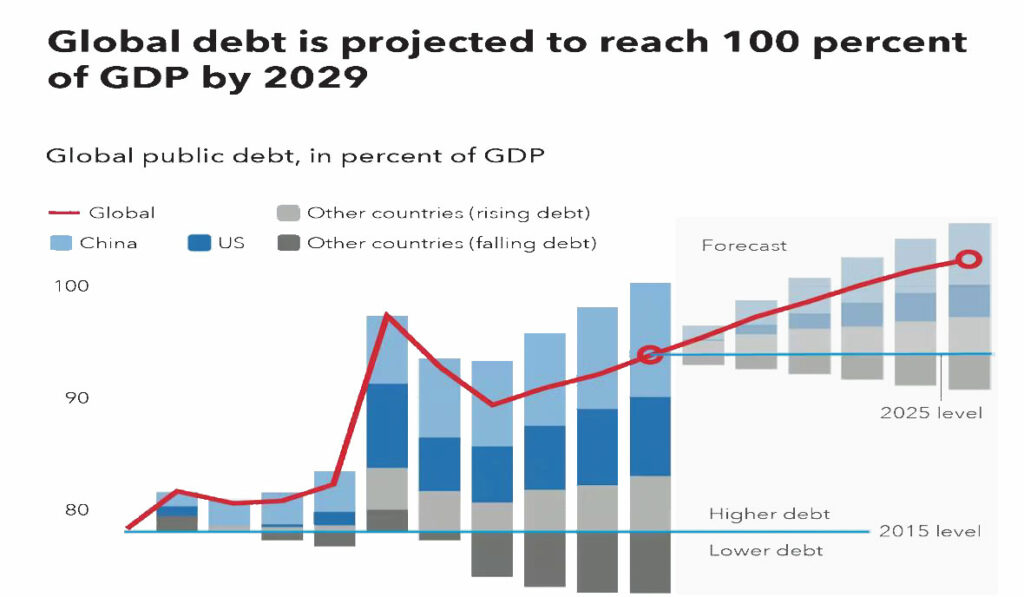

The global economic landscape is already fragile. Fiscal deficits linger around 5% of GDP, and public debt is nearing 100%. A significant portion of national income is simply consumed by interest payments. Many economies are still recovering from the pandemic, leaving them with severely limited capacity to respond to new shocks.

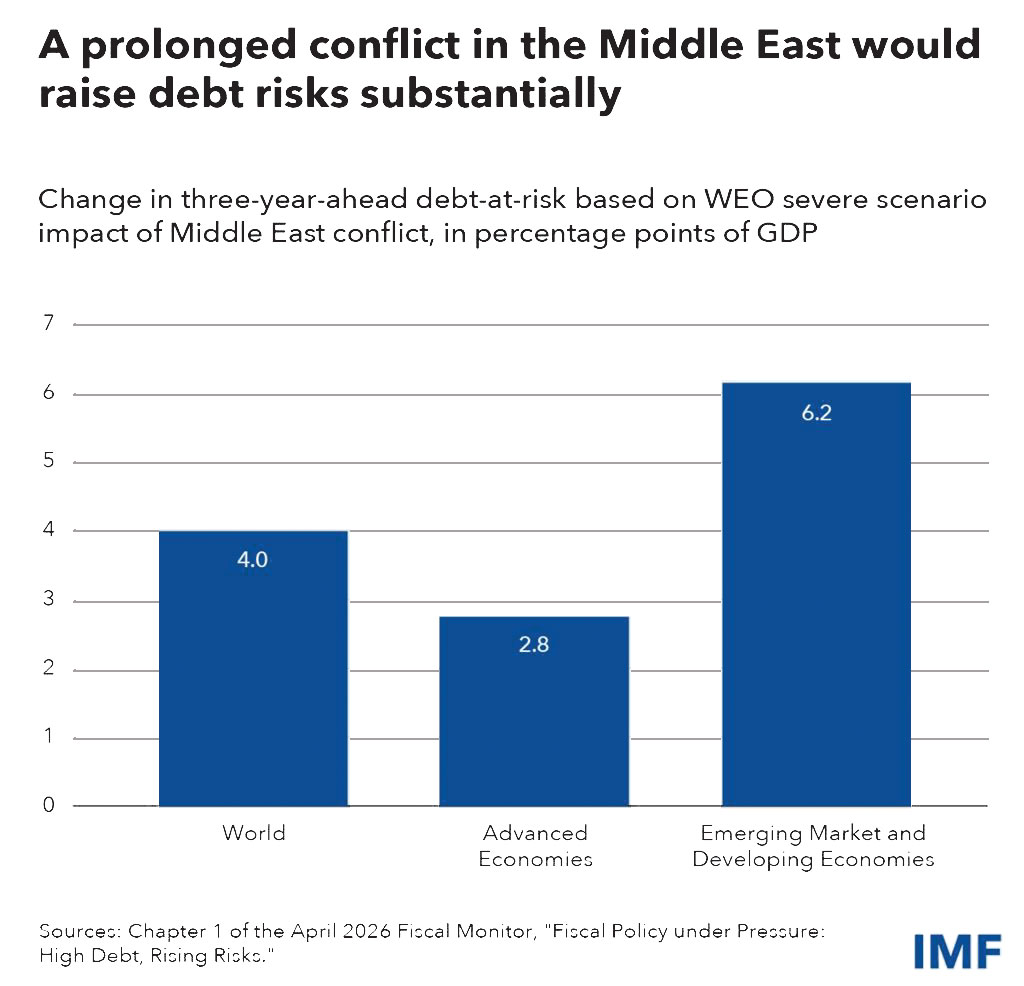

This isn’t a typical economic downturn. Nations are entering this crisis with dangerously little financial cushion. The Iran situation isn’t an isolated event; a severe escalation – a doubling of oil prices coupled with tighter financial conditions – could trigger a surge in debt vulnerabilities, particularly in emerging markets. Every financial decision must be carefully considered, precisely targeted, and designed for temporary impact.

Complacency is a dangerous trap. The International Monetary Fund warns that, under a severe scenario, debt levels could soar beyond 120% of GDP in emerging markets. What begins as an energy crisis can quickly spiral into a full-blown debt sustainability crisis. Short-term relief must be coupled with a credible, long-term plan for fiscal responsibility, or markets will react swiftly and harshly.

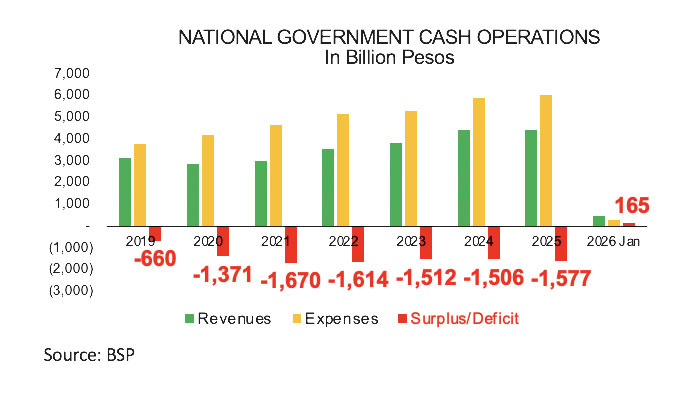

The Philippines is particularly exposed. Years of deficits exceeding P1.5 trillion have pushed public debt to around 63% of GDP, with interest payments consuming over 3% of the nation’s income. Crucially, significant investment is still needed in vital areas like infrastructure, poverty reduction, education, and healthcare. Compared to its neighbors in ASEAN, the Philippines’ fiscal position is among the weakest.

Fiscal discipline isn’t about harsh austerity measures. It’s about strategic prioritization – protecting stability today without sacrificing tomorrow. This requires three essential commitments: targeted and time-bound support for those most affected, reallocation of resources before resorting to further borrowing, and a firm commitment to long-term fiscal consolidation.

Fuel subsidies are a particularly contentious issue. While broad subsidies are costly, poorly targeted, and difficult to remove, a complete rejection in the Philippine context is unrealistic. The potential for widespread disruption and hardship is too great. The question isn’t whether to intervene, but how – through narrow, temporary, and well-targeted support for public transport and vulnerable commuters, avoiding blanket price suppression.

Inaction, or poorly conceived action, carries significant fiscal risks. Economic distress will lead to increased social protection spending, while weakened economic activity will reduce tax revenues. Reduced mobility and market distortions will further exacerbate the situation. Poorly designed austerity can be just as damaging as poorly designed subsidies.

Underlying all policy prescriptions is the critical need for good governance. Persistent concerns about corruption and inefficiency – exemplified by past scandals – undermine the effectiveness of any expenditure reallocation efforts. Without genuine reforms, fiscal space will continue to be eroded, public trust will diminish, and necessary adjustments will be blocked.

A credible fiscal response demands a shift from reactive spending to strategic policy design, guided by clear rules. This includes institutionalizing robust targeting mechanisms, enforcing spending discipline through rigorous audits, strengthening transparency and communication to build public support, adopting flexible fiscal rules with built-in safeguards, and mobilizing domestic revenue through tax reform.

This crisis extends beyond fiscal policy, requiring a coordinated, whole-of-government response encompassing energy diversification, monetary policy to control inflation, transport regulation to improve efficiency, and targeted social protection. The recently formed crisis committee is a positive step, but quicker, more responsive action is needed.

Relying on a single solution – either subsidies or austerity – will inevitably fail. The Philippines cannot afford either fiscal recklessness or paralysis. The path forward is narrow, demanding targeted support, disciplined spending, stronger governance, and a credible commitment to long-term fiscal consolidation. Failure to act decisively risks transforming a temporary external shock into a permanent fiscal crisis.