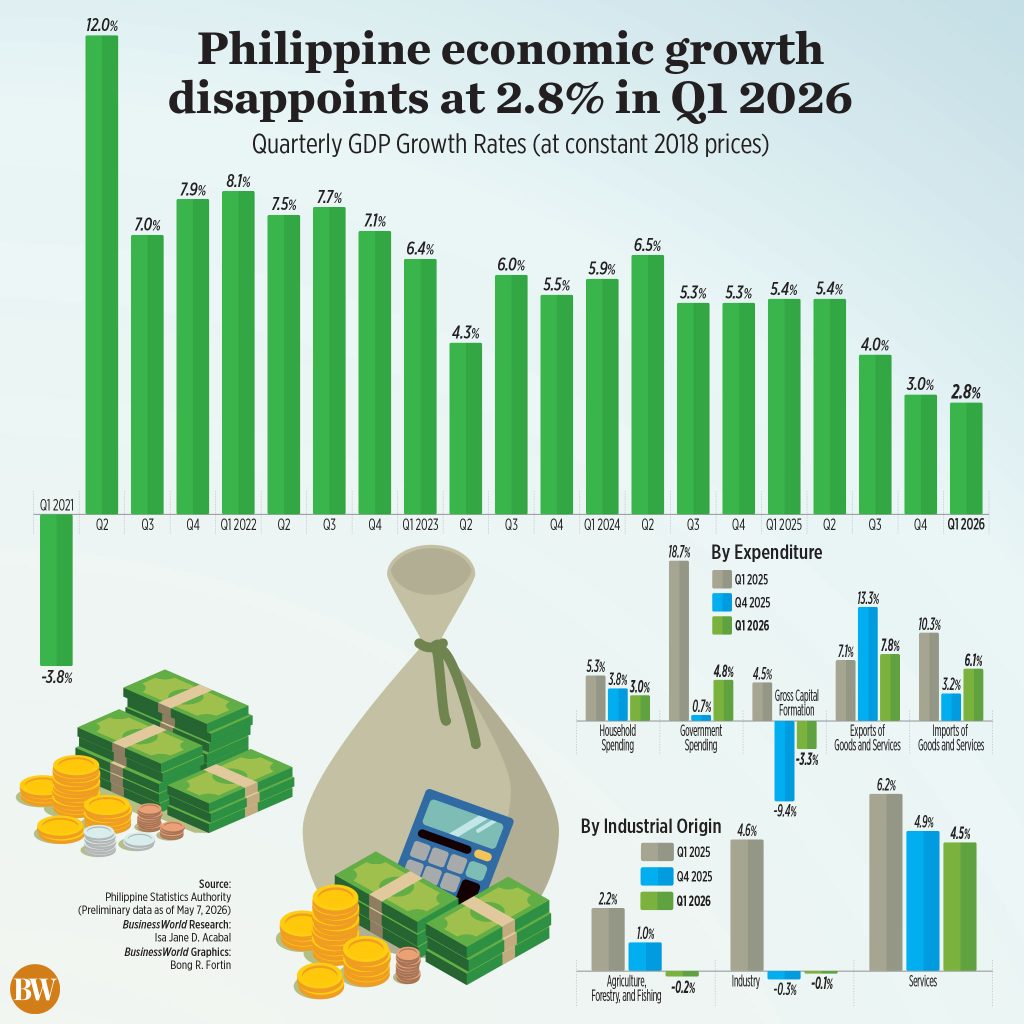

The Philippine economy just hit a nerve-wracking milestone—growth slowed to a mere 2.8% in the first quarter, the weakest since the pandemic crushed the world. A corruption scandal and soaring oil prices from the Middle East conflict are the culprits, slamming the brakes on economic activity.

Gross domestic product (GDP) expanded by just 2.8% from January to March, a dramatic drop from the 5.4% growth seen a year earlier. Economists had predicted 3.4%, but reality delivered a brutal miss—and even the revised 3% growth from the fourth quarter of 2025 looks optimistic now.

On a seasonally adjusted quarterly basis, GDP inched up 0.93% from 0.6% in the previous quarter. But that tiny gain can't mask the storm brewing beneath the surface.

The Department of Economy, Planning, and Development (DEPDev) admits the Middle East war, lingering effects of last year's corruption scandal, and delayed national budget releases all weighed heavily on the first three months. "We recognize that this outcome reflects the combined impact of significant domestic and global challenges," said Secretary Arsenio M. Balisacan.

"The conflict in the Middle East, which escalated toward the end of February, triggered higher global oil prices and renewed supply chain pressures, creating additional risks for oil-importing economies such as the Philippines," he added.

This 2.8% figure is the weakest since the 3.8% contraction in the first quarter of 2021—and if you exclude the pandemic, it's the slowest since the 1.8% growth in the fourth quarter of 2009. Neighboring economies like Vietnam, Indonesia, and China are outpacing the Philippines.

The Development Budget Coordination Committee will meet next Monday to review its macroeconomic assumptions, and Balisacan is blunt: "We don't expect to achieve the kind of growth that we expected to happen a year ago... we definitely will move our growth targets lower." The government's target range for the year was 5-6%—a distant dream now.

Household spending, the economy's main engine, grew at its weakest pace since the pandemic—just 3% annually, down from 5.28% a year ago. Excluding pandemic years, this is the slowest consumption growth since the third quarter of 2010.

The corruption scandal continues to poison consumer and business sentiment. "But I think that we are gradually moving out of that situation," Balisacan said, pointing to reforms toward accountability and transparency.

Government spending grew 4.8% in the first quarter—much slower than 18.7% a year ago, but a slight recovery from 0.7% in the fourth quarter. Oxford Economics' Jun Hao Ng sees this as a rebound from the scandal, and Balisacan expects spending to accelerate with catch-up programs.

Investment, measured by gross capital formation, contracted 3.3% from a year ago—driven by a 2.8% decline in construction, which itself was hammered by a 31.5% drop in government construction. "A breakdown of the data shows the main cause of the weakness was, once again, the flood control corruption scandal," said Gareth Leather, senior Asia economist at Capital Economics.

Construction has now dropped for three consecutive quarters since President Ferdinand R. Marcos, Jr. announced a crackdown on anomalous flood control projects in July. Exports rose 7.8%, while imports grew 6.1%—but that's cold comfort.

Services, which make up 63.2% of GDP, grew just 4.5%—their weakest since the pandemic. Agriculture shrank 0.2%, reversing last year's 2.2% growth. Industry contracted 0.1%, another reversal from 4.6% growth a year ago. The numbers tell a story of stagnation across every sector.

Is this stagflation? Balisacan says no—pointing to textbook definitions that require high inflation, stagnant growth, and high unemployment simultaneously. But analysts disagree. "The Philippines is going through a period of stagflation," Leather argued, citing slowing growth and rising inflation.

Chinabank Research warned of a "twin-crisis squeeze," with growth weakened by the corruption controversy and strained by surging oil and food prices. Metropolitan Bank & Trust Co.'s Nicholas Antonio T. Mapa noted the economy was losing momentum even before the corruption probe and Middle East conflict, due to "private underinvestment and a buildup in household debt."

Inflation averaged 2.8% in the first quarter, but April's print hit 7.2%. With the Bangko Sentral ng Pilipinas signaling more rate hikes—including a 25-basis-point hike in April to bring the policy rate to 4.5%—the economy faces an uphill battle. ING's Deepali Bhargava believes weak GDP won't deter a June rate hike.

ANZ Research summed it up: "Overall, risks to near-term growth remain skewed to the downside, particularly if inflation stays elevated or global geopolitical conditions deteriorate." The Philippines is walking a tightrope—and the rope is fraying.