A chilling wave of pessimism has gripped the Philippine business community, plunging confidence to its lowest level in over a quarter-century. March saw a dramatic shift, with firms bracing for economic headwinds fueled by escalating tensions in the Middle East and the resulting surge in fuel costs.

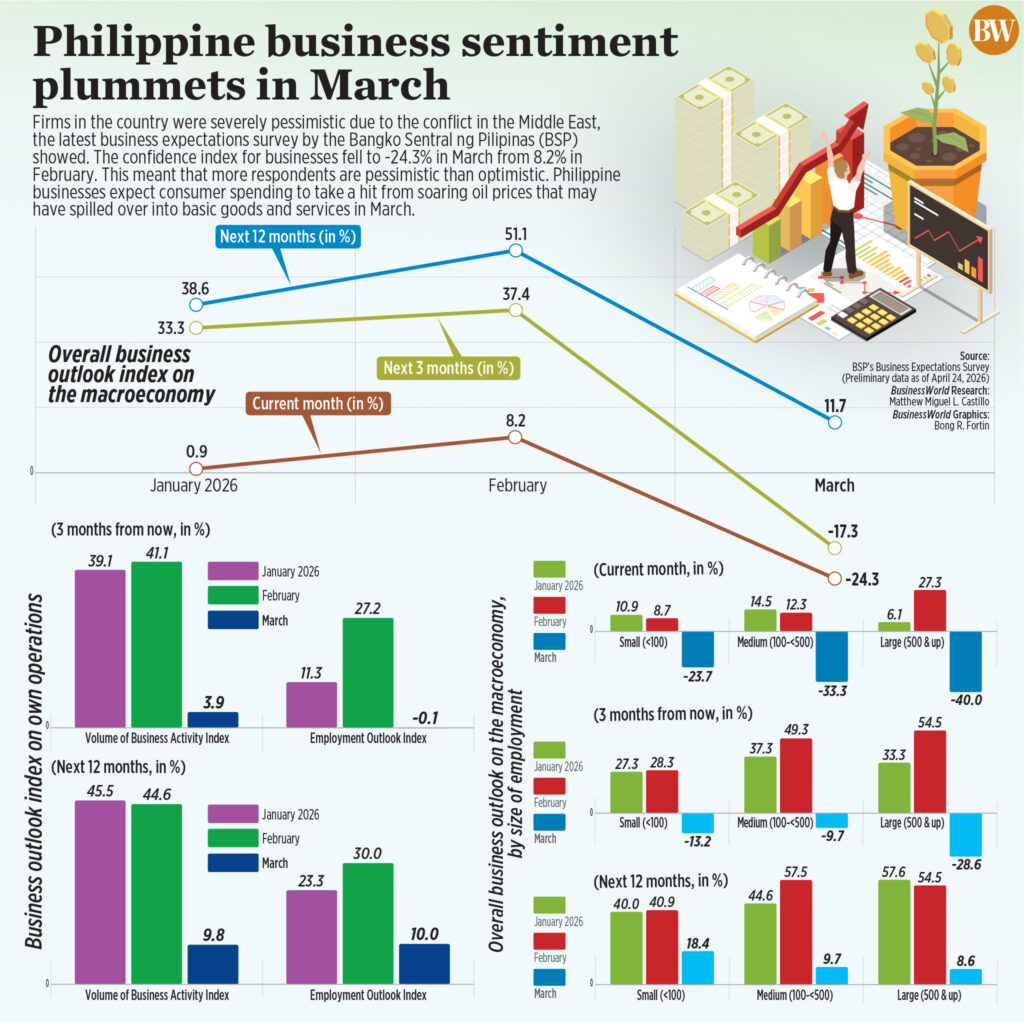

The central bank’s latest survey revealed a current-month confidence index plummeting to -24.3%, a stark contrast to February’s 8.2%. This isn’t merely a slight dip; it signifies a critical mass of businesses now anticipating tougher times ahead, a sentiment not seen since the economic turmoil of 2001.

The root of this anxiety lies in the unfolding crisis abroad. The conflict’s impact on global energy markets, particularly the disruption of vital shipping lanes, has sent domestic pump prices soaring. Businesses fear this will trigger a ripple effect, eroding consumer spending as the cost of essential goods and services climbs.

This pessimism isn’t limited to the immediate future. The outlook for the second quarter has also turned negative, and even longer-term projections for the rest of the year have dimmed. Businesses are bracing for a prolonged period of economic uncertainty, anticipating the adverse effects of the Middle East conflict will linger.

Financial strain is a growing concern. Firms foresee tighter access to credit and a worsening cash position, reflecting a broader tightening of financial conditions. This creates a challenging environment for investment and expansion, potentially stifling economic growth.

Despite these challenges, some sectors show resilience. Capacity utilization in industry and construction has risen, and the electricity sector is experiencing a seasonal boost. However, these pockets of activity are overshadowed by the pervasive anxieties surrounding rising costs and dwindling consumer demand.

Businesses are grappling with a complex web of obstacles: fierce competition, insufficient demand, and high interest rates. Now, the escalating oil prices, a direct consequence of the Middle East conflict, are adding another layer of pressure, driving up production costs across the board.

The labor market is also feeling the impact. Employment outlooks have turned negative for June and the year ahead, signaling a potential slowdown in hiring. While some companies still have expansion plans in the pipeline, the overall trend points towards caution and restraint.

Adding to the economic concerns, businesses anticipate further depreciation of the Philippine peso, forecasting an average rate of P59.60 in June and P60 over the next 12 months. They also expect borrowing rates to increase, further compounding the financial pressures on businesses.

Inflationary pressures are intensifying. Businesses now expect inflation to average 2.8% in March, rising to 3.1% in June and 3.3% in the next 12 months. This upward trend has prompted the central bank to revise its inflation forecasts upwards, projecting 6.3% for the year and 4.3% for the next.

Interestingly, a separate survey revealed a glimmer of optimism among consumers in the first quarter, conducted *before* the recent escalation of the Middle East conflict. Consumer confidence, while still negative, improved slightly, driven by expectations of higher earnings and stable employment.

However, even consumer sentiment is showing signs of weakening. The outlook for the coming quarters is less upbeat, reflecting concerns about government corruption, rising inflation, and ineffective policies. This suggests that the positive sentiment observed in the first quarter may be short-lived.

The surveys paint a complex picture: a business community deeply concerned about the unfolding global crisis and its impact on the Philippine economy, coupled with a consumer base that, while initially optimistic, is growing increasingly wary of the challenges ahead. The coming months will be critical in determining the extent of the economic fallout.