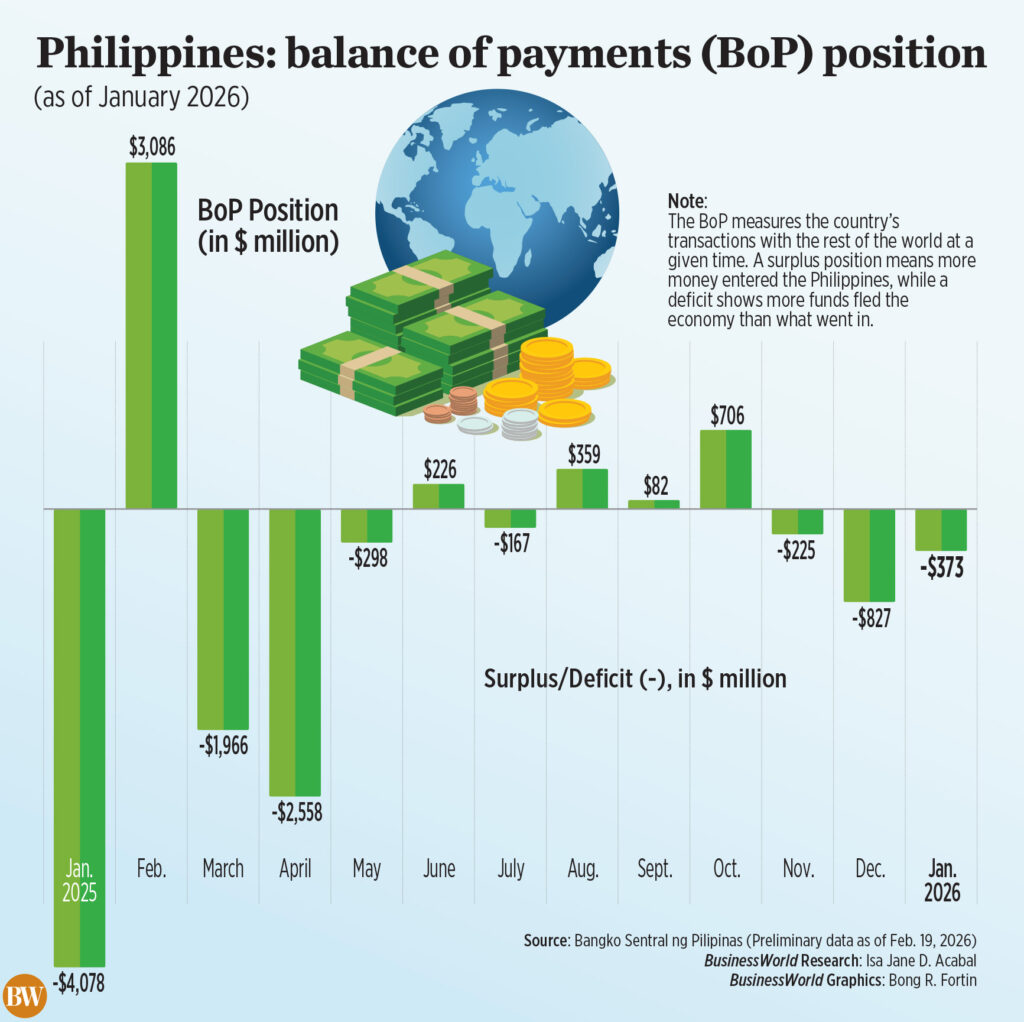

The Philippines experienced a significant shift in its economic standing in January 2026, with the balance of payments deficit narrowing dramatically to $373 million. This represents a stark contrast to the $4.078 billion gap recorded during the same period last year, signaling a positive, though complex, change in the nation’s financial interactions with the world.

This deficit, while marking the third consecutive month of shortfall, is considerably smaller than the $827 million recorded just the previous December. Experts attribute this improvement to a combination of factors, including seasonally high import payments and the outflow of profits at the start of the year, coupled with strategic adjustments in investment portfolios amidst global economic uncertainty.

The core of the issue lies in the country’s trade balance: imports continue to exceed exports. This dynamic reflects robust domestic demand fueled by infrastructure projects, while global appetite for Philippine exports and service industries, like business process outsourcing and tourism, remains subdued. However, analysts emphasize this isn’t a cause for alarm.

Despite the deficit, the Philippines’ external financial buffers remain remarkably strong. The trade deficit itself has been shrinking, ending 2025 at its lowest point in four years – a $49.17 billion shortfall, a 9.5% improvement over 2024. This suggests underlying economic health and resilience.

Looking ahead, experts predict a stabilization of the balance of payments as remittance inflows from overseas workers increase and tourism rebounds. The trajectory will be heavily influenced by global oil prices, the performance of electronics exports, and the direction of interest rates in the United States.

Crucially, attracting long-term investments and boosting export competitiveness are seen as key strategies for sustained improvement. Simply reacting to the headline deficit number is insufficient; a focus on fundamental economic strengths is paramount.

Adding to the positive outlook, the Philippines’ foreign reserves surged to a 16-month high of $112.6 billion at the end of January. This represents the highest level since September 2024 and a nearly 1.6% increase from December, bolstering the nation’s financial security.

These reserves are more than sufficient to cover 7.5 months’ worth of imports and service payments, significantly exceeding the standard three-month benchmark. They also provide a substantial cushion against external debt, covering approximately 4.1 times the country’s short-term obligations.

These reserves, comprised of foreign-denominated securities, foreign exchange, and gold, are vital for financing imports, managing debt, stabilizing the currency, and protecting the Philippines from global economic shocks. The central bank projects reserves to remain around $110 billion by the end of the year.