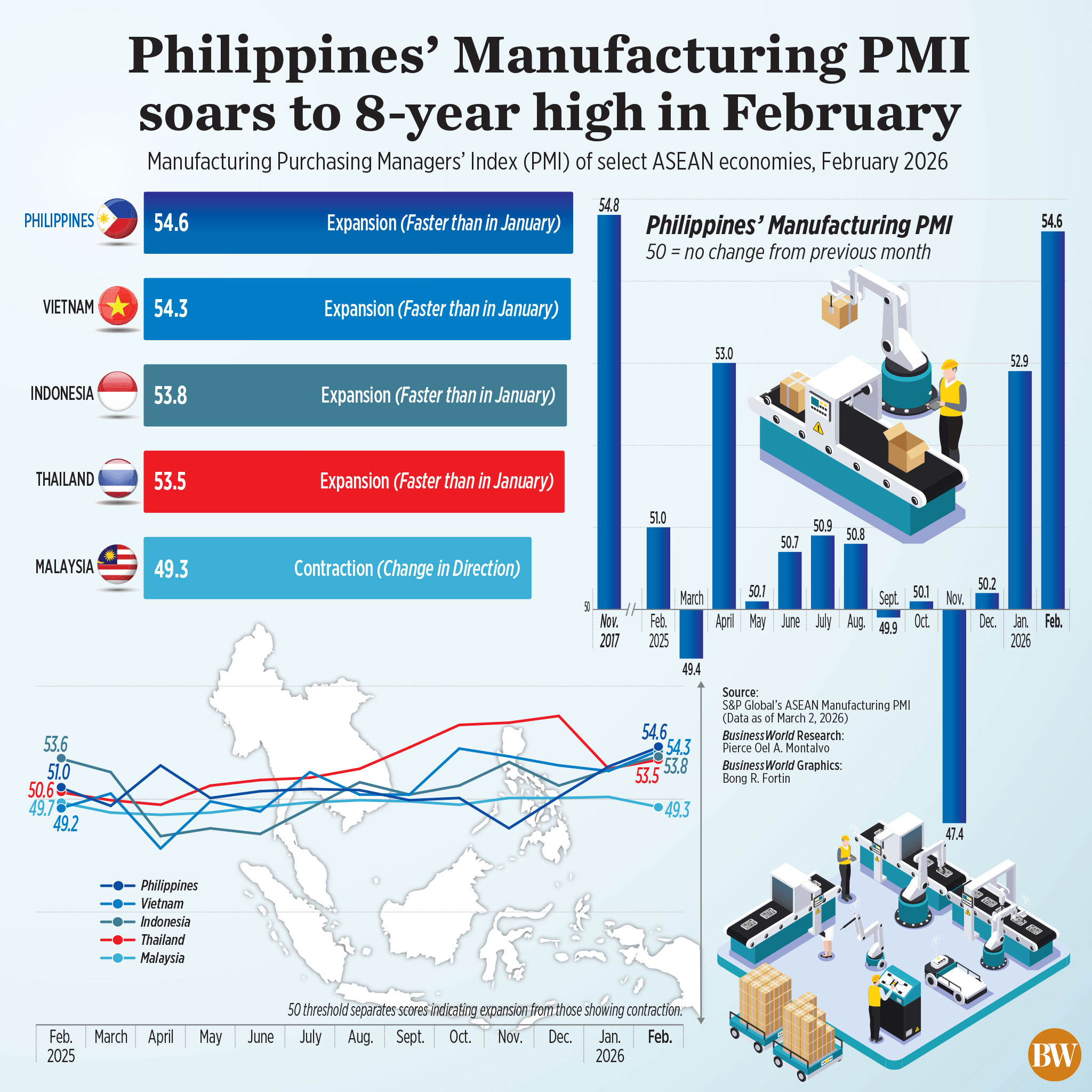

Philippine manufacturing surged to an eight-year high in February, signaling a powerful start to 2026. The S&P Global Philippines Manufacturing Purchasing Managers’ Index (PMI) leaped to 54.6, a level not seen since November 2017, indicating a significant acceleration in factory activity.

This impressive growth wasn’t a subtle shift; it was a dramatic influx of new orders fueling a robust expansion in output. Both measures reached multi-year peaks, painting a picture of a sector brimming with momentum and confidence.

The Philippines didn’t just perform well regionally – it led the way. Compared to its ASEAN neighbors, the nation’s manufacturing expansion outpaced Vietnam, Indonesia, and Thailand, while Malaysia experienced a contraction.

Underlying this success was a remarkable surge in business confidence. Manufacturers expressed optimism about continued demand, anticipating further production increases and a sustained period of growth.

For the third consecutive month, operating conditions improved across the Philippine manufacturing landscape. Factories reported faster increases in both production volumes and new orders, building on gains made in previous months.

The demand was palpable. New orders soared to their highest level in over eight years, driven by a combination of new clients and bulk purchasing from existing customers. Both domestic and international demand contributed to this impressive growth.

This heightened activity translated into sustained job growth, with manufacturers increasing staffing levels for the second month in a row. However, the pace of hiring wasn’t quite enough to keep up with the rising tide of work, leading to a buildup of backlogs.

Manufacturers also ramped up their input buying, recording the fastest expansion rate since January 2025. Despite this, increased activity, coupled with adverse weather and port congestion, led to longer delivery times for essential materials.

Interestingly, despite these logistical challenges, operating expenses actually fell in February. This allowed manufacturers to reduce their charges, potentially further stimulating demand and bolstering competitiveness.

Looking ahead, manufacturers expressed a significantly improved outlook for the next twelve months. This renewed confidence stemmed from expectations of continued improvements in underlying demand trends.

However, a shadow looms on the horizon: the potential for rising oil prices. Escalating tensions in the US-Iran conflict could trigger a spike in energy costs, posing a risk to the manufacturing sector’s continued expansion.

Recent increases in fuel prices – gasoline up for eight consecutive weeks, diesel and kerosene for ten – already demonstrate a growing pressure. The impact on manufacturing will depend on the duration and severity of the conflict and how oil suppliers manage the risk.

While global tariffs haven’t strongly impacted the sector yet, reflected in below-50 price indicators, manufacturers have been strategically suppressing prices to support export growth and capitalize on new orders. This delicate balance could be disrupted by rising oil costs.

Despite this uncertainty, the February data reveals a manufacturing sector that is currently thriving, demonstrating resilience and a clear upward trajectory. The coming months will be crucial in determining whether this momentum can be sustained in the face of external pressures.