A nagging sore on my leg. That’s how it started. A small, persistent irritation that refused to heal, soon joined by others – blemishes that appeared and stubbornly remained. My primary care physician, Dr. Andrew Diamond, wisely suggested an antibiotic wash and a referral to a dermatologist.

The initial specialist was out of network, a common healthcare hurdle. But a quick request to One Medical, and I was swiftly directed to an in-network dermatologist, Dr. Cristian Gonzalez, complete with pre-authorization from Blue Shield. It felt like a small victory in a system often designed to confuse.

Dr. Gonzalez quickly assessed the situation, then expertly went to work – injecting, freezing, and directly treating each lesion. He prescribed a simple, inexpensive topical steroid, and over four visits spanning the summer and fall, my legs began to heal, returning to a remarkably smooth condition.

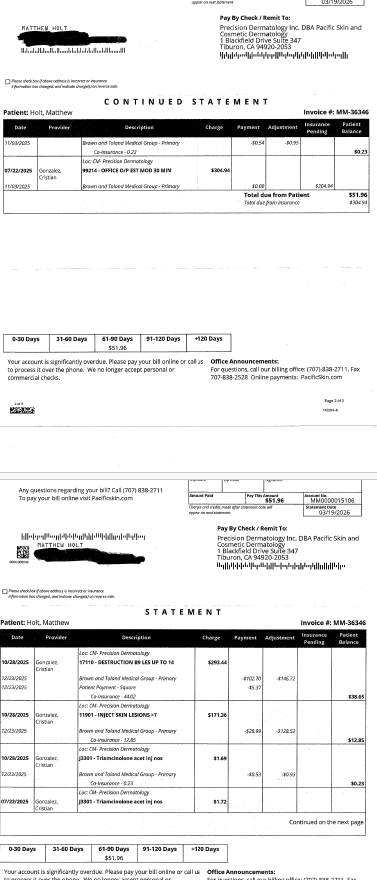

Each visit involved a standard $85 co-pay, dutifully paid with my HSA card. There was one brief, dismissed inquiry about a balance due, quickly explained away as an error. Until now. Four months after my final appointment, a bill for $51.96 arrived in the mail.

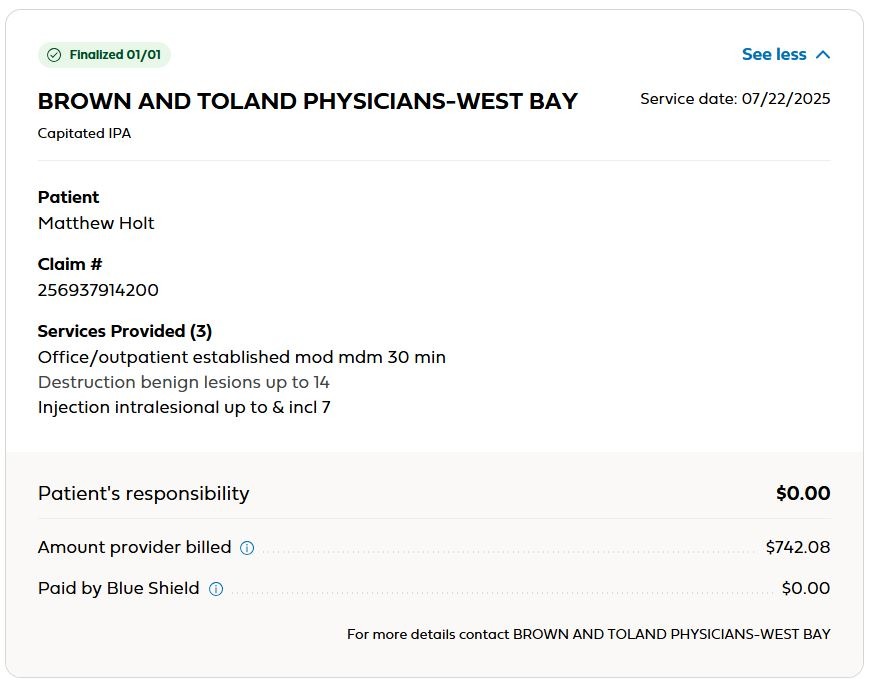

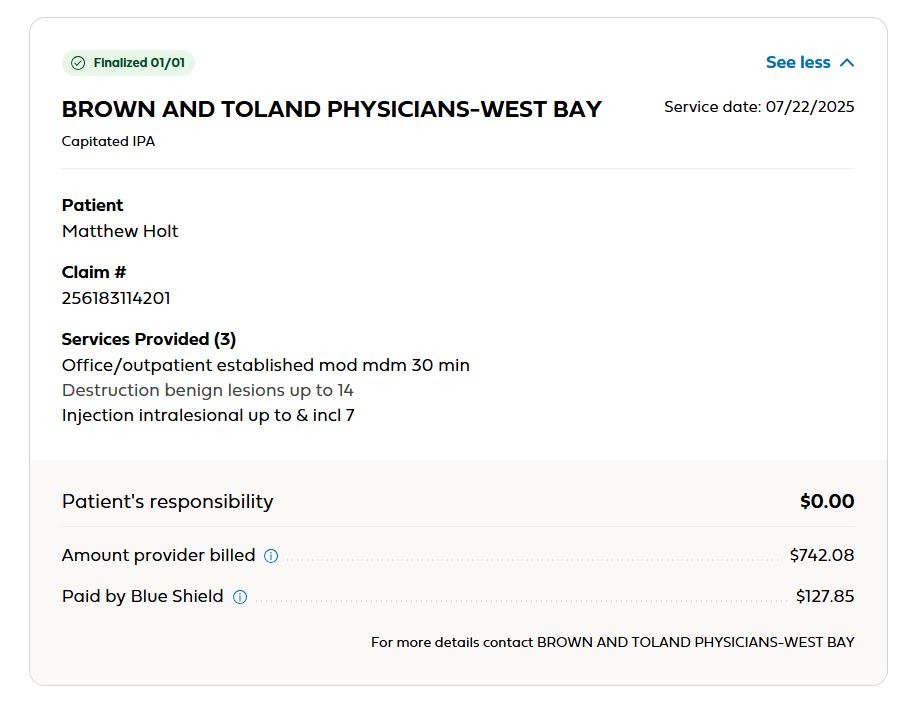

The confusion began with my Explanation of Benefits (EOBs) from Blue Shield. Each visit had generated *three* identical claims, resulting in three nearly identical EOBs. Two claims appeared to be paid, one remained outstanding. It was a perplexing pattern of duplicated paperwork.

The total paid per visit seemed to be around $255, plus my $85 co-pay. But then there was a separate claim for a drug administered during one visit – a minuscule charge of $1.72. Blue Shield only paid $1.20, leaving me responsible for the remaining 52 cents. Even with the co-pay already covered, a portion of the drug cost was somehow still my burden.

My benefits summary confirmed specialist co-pays had increased to $90, but made no mention of co-insurance for in-office drugs. The 52-cent charge, however, represented roughly 30% of the total cost – a common co-insurance rate for certain healthcare services, even within an HMO. It seemed I was being billed for a portion of the injected medication, separate from the office visit itself.

This pattern repeated across multiple visits. I’d paid my $85 co-pay, Blue Shield issued an EOB, and Pacific Dermatology billed around $600, receiving approximately $170 in payment. Was my co-pay included in that $170? It was unclear. Then came the final visit, the one that finally resolved the issue, followed by the $51.96 bill months later.

I contacted the billing service, speaking with a helpful representative named Terry Anderson. He explained that Brown & Toland, the IPA managing my Blue Shield plan, had recently undergone system changes, creating a backlog of billing complexities. He indicated I owed co-insurance on the October visit, despite already paying a co-pay.

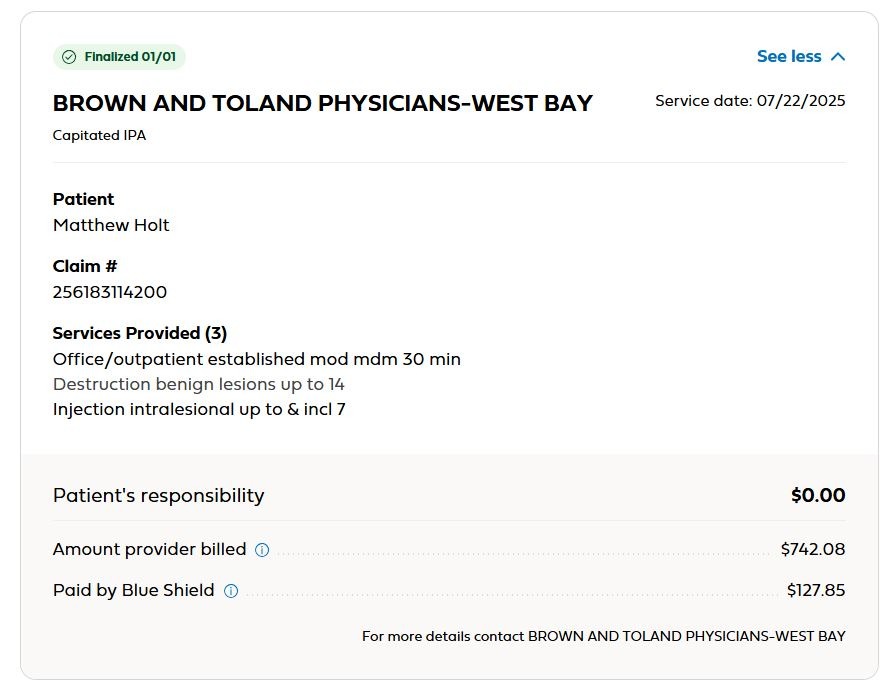

The EOB from Brown & Toland revealed a significant discrepancy. The original $304.94 charge for the office visit wasn’t even on the bill I received. It had been adjusted down to $152.47, with Blue Shield paying $62.47 and my $85 co-pay covering the remainder. I had, in effect, paid more than Blue Shield for the same service.

Further charges for “destruction of lesions,” “injection of lesions,” and the drug itself were also adjusted downwards. However, this time, Blue Shield only covered 70% of the adjusted amount, leaving me with a 30% co-insurance payment. The same co-insurance structure applied to inpatient visits was now being applied to routine dermatology care.

The process felt needlessly convoluted. During each brief appointment – a quick consultation with a physician’s assistant followed by a 10-minute visit with Dr. Gonzalez – a substantial amount of money was changing hands. A total of $330 received for a 15-minute visit equates to a remarkable hourly rate.

The financial mechanics of the visit were baffling. Why were three claims submitted for a single service? Why were different amounts billed for essentially the same treatment? And why was the drug being billed separately? The entire system seemed designed to obscure, rather than clarify, the true cost of care.

The layers of administration – the billing company taking a cut, Brown & Toland adding its markup – all contributed to the escalating costs. Even the smallest charges, like the 52-cent co-insurance, added up, highlighting the inefficiency of a fee-for-service model. It was the doctor’s professionalism, and my own sense of being cured, that ultimately ended the cycle.

This experience underscored a fundamental question: could these minor dermatological issues be effectively managed within a primary care setting? The visits were brief, requiring specialized expertise but not extensive diagnostic testing. Perhaps a more integrated approach, similar to models like Kaiser Permanente, could streamline care and reduce costs.

Ultimately, this wasn’t about the money. It was about the sheer irrationality of the system. There is no logical explanation for the complexity and confusion surrounding something as simple as treating a few blemishes.