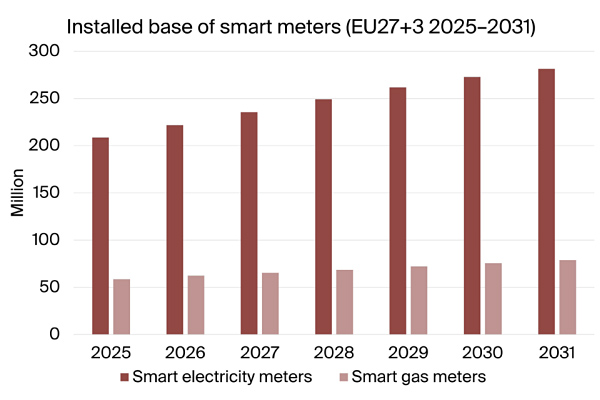

By the end of 2025, roughly two‑thirds of electricity customers in the EU27+3 region had a smart meter installed, representing about 209 million units. The market is projected to expand at a compound annual growth rate of 5.1 percent, reaching approximately 85 percent penetration by 2031.

During the 2025‑2031 period, more than 131 million new smart electricity meters are expected to be deployed. A sizable share of this demand will arise from first‑generation rollouts in countries such as Germany, the United Kingdom, Poland and Greece, while replacement and second‑generation projects will drive shipments in Spain, France and the Netherlands.

The forecast distinguishes two distinct phases: initial large‑scale installations and subsequent refresh cycles. First‑generation meters are anticipated to account for 65 percent of cumulative shipment volumes throughout the forecast horizon.

Central and Eastern Europe, together with Southeastern Europe, are slated to generate 76 percent of all first‑generation shipments by 2031. These regions remain in the early stages of coverage, whereas mature Western European markets are shifting focus toward upgrading existing meter estates.

This split creates divergent business environments for equipment manufacturers and system integrators. Suppliers targeting low‑penetration markets must address cost and coverage challenges, while those operating in mature markets need to support interoperability and migration risk management.

Communications technology choices are equally pivotal. Standalone wireless solutions are gaining traction and are expected to represent over half of annual shipment volumes, peaking at about 62 percent in 2028.

3GPP‑based low‑power wide‑area (LPWA) technologies, particularly LTE‑M and NB‑IoT, are the primary drivers of this shift, with annual shipments of LPWA‑enabled electricity meters projected between 2.4 million and 6.1 million units from 2025 to 2031.

Despite the rise of cellular LPWA, powerline communications (PLC) will continue to play a significant role, especially in countries preparing second‑generation rollouts that build on existing PLC infrastructure. Some markets may adopt upgraded or hybrid PLC approaches to meet new performance requirements.

For connectivity providers, the implication is clear: a multi‑technology strategy remains essential. Cellular LPWA can reduce reliance on dedicated utility networks, but PLC retains value where utilities have already invested and where continuity of operations is critical.

Smart gas metering is also expanding, with the installed base expected to grow from nearly 59 million units in 2025 to around 79 million by 2031, achieving roughly 48 percent penetration.

The broader rollout of smart meters will gradually increase the availability of granular consumption data for enterprises and industrial energy users, though the impact will depend on national regulations and utility data‑access policies.

Overall, Europe’s smart‑metering market remains large but is becoming increasingly segmented by region, deployment phase, and technology choice, shaping a complex landscape for manufacturers, integrators, and IoT solution providers.