The cellular IoT market has experienced a significant recovery in 2025, with shipments reaching 612 million units and revenues totaling US$5.6 billion. This growth, however, has been accompanied by a widening gap between unit growth and revenue growth, indicating that pricing power remains uneven.

New data from Berg Insight reveals that annual shipments of cellular IoT modules increased by 33 percent in 2025, while revenues rose by 19 percent. The figures exclude automotive NAD modules, which are treated as a separate segment due to their unique supply chains and pricing dynamics. Despite the strong growth, average revenue per shipped module declined year-on-year, suggesting that demand has recovered, but pricing power remains uneven.

The rebound in the market is attributed to stronger demand across all major regions, following a period of weaker sales caused by elevated customer inventories. Additionally, local policies in countries such as Spain and China have contributed to the growth, driven by smart metering, payments, utilities, public infrastructure, and compliance-led device refresh cycles.

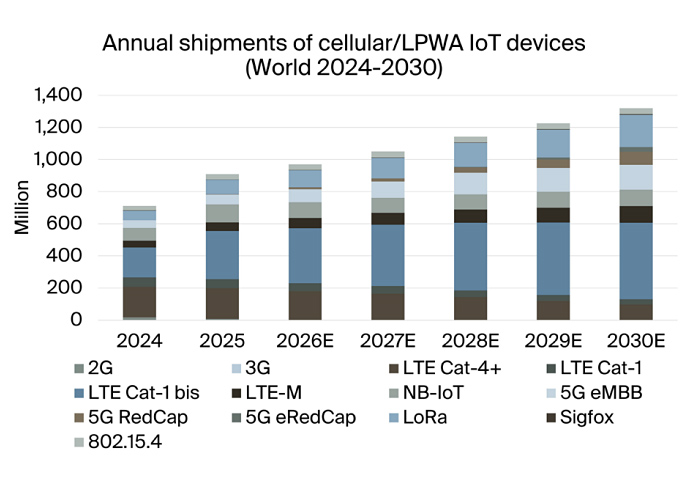

Berg Insight forecasts cellular IoT module shipments to grow at a compound annual growth rate of 7 percent through 2030, reaching 878 million units. This outlook suggests a normalization of growth after the post-inventory rebound, but also highlights the growing pressure on module pricing and component costs.

The market is facing a new challenge with memory pricing becoming a mounting constraint. Memory manufacturers are allocating more production capacity to high-bandwidth memory for AI servers and data centre infrastructure, creating an unusual cross-market pressure point. Cellular IoT modules are indirectly exposed through shared semiconductor supply chains, leading to price pressure rather than outright shortages.

As a result, module pricing is becoming less static, with vendors introducing periodic price reviews and contractual mechanisms to manage component cost volatility. This can complicate long-cycle product planning for OEMs and system integrators, especially where device business cases depend on stable bill-of-materials costs over multi-year deployments.

The competitive structure of the module market remains concentrated, with Berg Quectel, Fibocom, Telit Cinterion, MeiG, and China Mobile IoT accounting for 73 percent of cellular IoT module revenues in 2025. However, the volume leadership is strongly shaped by China's domestic market, with Quectel, China Mobile IoT, Sunsea AIoT, Lierda, and Fibocom emerging as leading vendors by volume.

The chipset picture reinforces the same regional dynamic, with China-based chipset vendors reporting solid growth in LTE Cat-1 bis and NB-IoT. Qualcomm retained a substantial position in LTE-M, high-end 4G LTE, and 5G eMBB chipsets. The report underscores a more fragmented planning environment for connectivity providers and enterprises, with low-cost cellular IoT categories continuing to scale, 5G module economics being more exposed to memory pricing, and vendor choice increasingly depending on the target application, geography, and technology tier.