The Philippine economy faced significant headwinds in the first quarter, with growth likely slowing compared to the previous year. Economists point to a complex interplay of factors – strained household budgets, cautious government spending, wavering business confidence, and a surge in global energy prices fueled by escalating tensions in the Middle East – as key contributors to this deceleration.

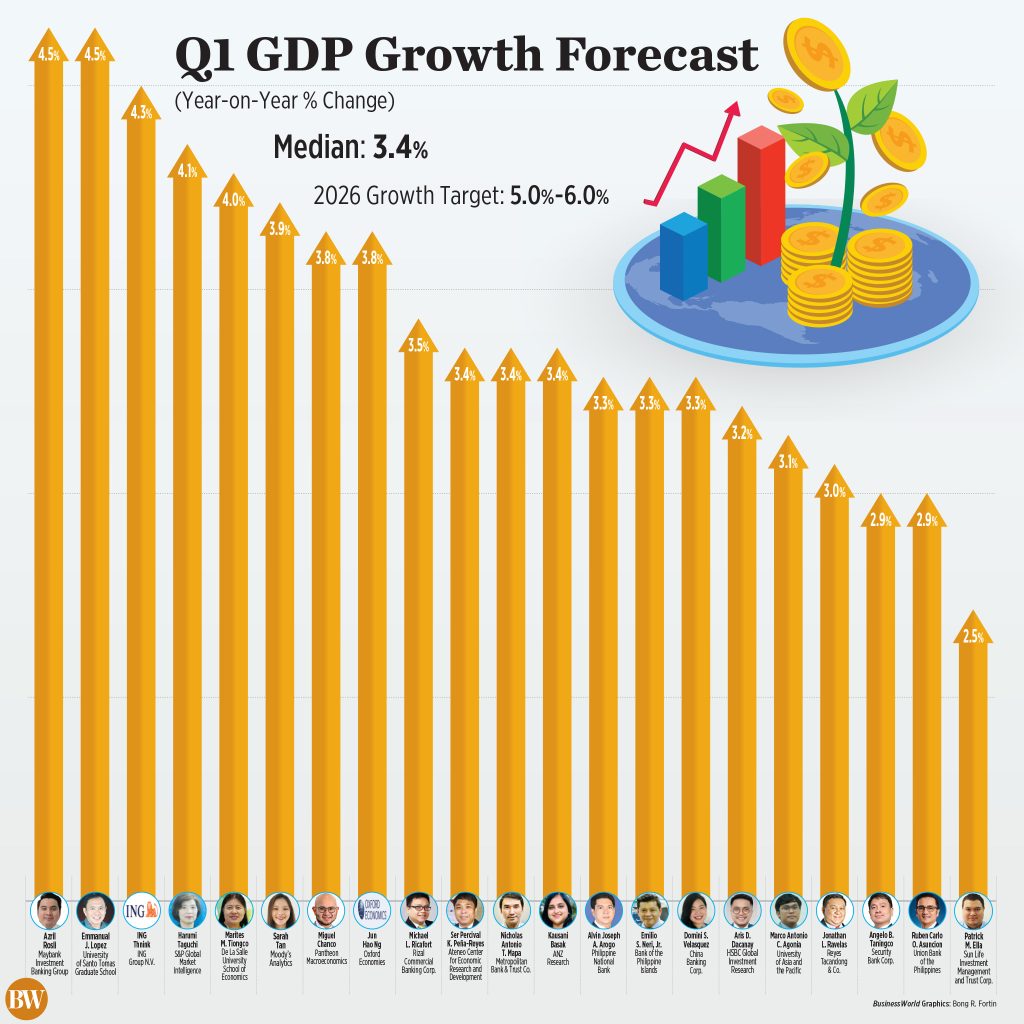

Initial forecasts suggest a GDP growth of 3.4% for January to March, a figure that, while exceeding the fourth quarter of 2025’s 3% growth, falls short of the government’s 5-6% target. This potential slowdown underscores the delicate balance facing the nation as it navigates a challenging global landscape.

A primary concern is the erosion of household purchasing power. Consumers are increasingly focused on managing debt and coping with rising energy costs, leading to a moderation in spending. This trend is compounded by a slowdown in government expenditure and a lingering hesitancy in investment, still feeling the effects of previous monetary policy adjustments.

The conflict in the Middle East casts a long shadow, directly impacting the Philippines as a net importer of crude oil. Disruptions to global oil supplies have driven prices up sharply, creating a ripple effect throughout the economy. This energy shock is already influencing behavior, with more people opting for work-from-home arrangements and adjustments in public transportation.

Inflationary pressures are intensifying, accelerating to 4.1% in March – the fastest pace in nearly two years. This surge, driven by rising fuel and freight costs, is squeezing household budgets and impacting the affordability of essential goods. The central bank now anticipates inflation averaging 6.3% this year, exceeding its target range.

Beyond energy prices, a recent scandal involving flood control projects has further dampened confidence, adding to the economic headwinds. Government underspending in the first quarter, particularly in infrastructure, is expected to further constrain growth, lacking the multiplier effect that robust public investment could provide.

Looking ahead, economists predict the second quarter will likely feel the full force of the oil shock. A further slowdown to between 3.6% and 4.2% is anticipated as higher costs for food, transportation, and electricity continue to erode consumer spending. The persistence of these inflationary pressures, alongside the pace of government spending and policy adjustments, will be critical determinants of the nation’s economic trajectory.

Strategies to mitigate these challenges include diversifying oil import sources and potentially implementing targeted fuel subsidies. However, fiscal constraints may limit the scope of such programs. The coming months will be a crucial test of the Philippines’ resilience as it confronts these interconnected economic pressures.