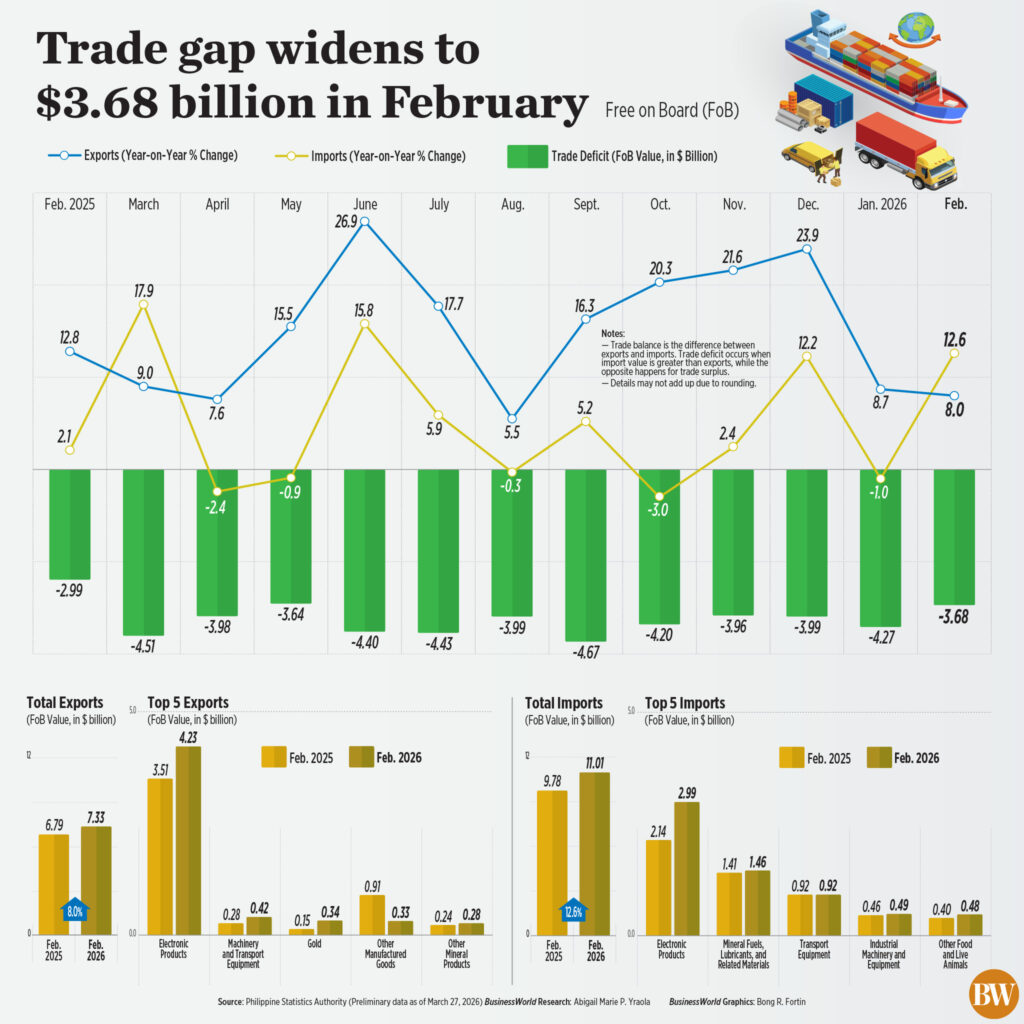

February’s trade figures revealed a widening gap between the Philippines’ imports and exports, a signal of economic currents shifting beneath the surface. Imports surged, climbing by a significant 12.6% compared to the previous year, while export growth slowed, painting a complex picture of the nation’s economic health.

This expanding trade deficit – reaching $3.68 billion – isn’t necessarily a cause for alarm, but a stark reminder of the Philippines’ vulnerability to global forces. Analysts point to escalating energy prices, fueled by ongoing conflict in the Middle East, as a primary driver of this trend, threatening to disrupt the delicate balance of economic recovery.

The surge in imports wasn’t across the board. While overall figures rose, purchases of essential raw materials and intermediate goods actually *decreased* by 13.7%. The real growth came from capital goods – machinery and equipment – leaping by an impressive 55.5%, and a notable increase in consumer goods, suggesting strengthening domestic demand and ongoing investment.

On the export side, the 8% year-on-year increase, while positive, represented a deceleration from previous months. The electronics sector, the backbone of Philippine exports, continued to contribute significantly, but even its growth showed signs of moderating. Concerns are mounting that global demand for these key products may be softening.

Looking ahead, the shadow of the Middle East conflict looms large. Rising oil prices are expected to further inflate import costs, potentially widening the trade deficit in the coming months. This isn’t just about numbers; it translates to higher costs for businesses and consumers alike, impacting everything from transportation to production.

However, experts suggest this initial price-driven import surge may be temporary. A potential slowdown in global demand, coupled with possible supply shortages, could correct the imbalance later in the year. The key will be navigating these turbulent waters and adapting to a changing global landscape.

The United States remains the Philippines’ primary export destination, with a substantial 19.3% share of total sales. However, a diversification of trade partners is evident, with increased shipments to East Asia and the European Union, a strategic move to mitigate risks associated with reliance on a single market.

Beyond immediate concerns, long-term strategies are crucial. Economists emphasize the need for improved trade facilitation, streamlined logistics, and increased investment in key manufacturing sectors. Strengthening local supply chains and maintaining macroeconomic stability are also vital to weathering future external shocks.

The coming months will be critical. March’s trade performance will hinge on a complex interplay of factors – oil prices, global electronics demand, exchange rate fluctuations, and even seasonal trade patterns. The Philippines faces a challenging path, but one that can be navigated with strategic planning and proactive policy adjustments.