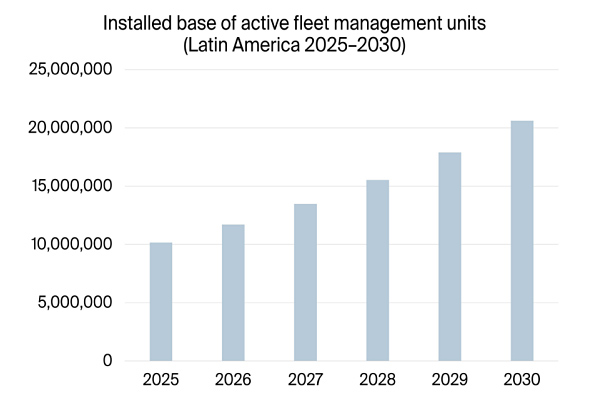

The installed base of fleet management systems in Latin America is expected to reach 20.6 million units by 2030, indicating a significant addressable market for telematics connectivity, platforms, and lifecycle services in the region. This forecast highlights the growing demand for connected vehicles and the need for companies to manage, bill, secure, and integrate these vehicles into business processes over time. The installed base of fleet management systems is a key indicator of the IoT ecosystem's growth in Latin America. The figure represents a large operational footprint of connected vehicles that will require ongoing management and support.

The focus on installed systems rather than new device shipments or platform features sets this forecast apart from typical industry announcements. In the telematics sector, installed base data is more closely tied to recurring service revenues and operational complexity than shipment numbers. For companies providing connectivity, 20.6 million active fleet management units imply a substantial base of SIMs, data plans, and roaming or multi-network arrangements. This will drive demand for device onboarding, vehicle data normalization, maintenance workflows, driver behavior analytics, and customer support.

The forecast underlines the complex nature of fleet IoT in Latin America, where fleet management systems intersect with logistics, fuel costs, security, maintenance, compliance, and driver productivity. As adoption expands, the challenge will shift from proving the value of tracking to integrating vehicle data into dispatch, insurance, finance, maintenance, and customer-facing systems. This integration will require companies to develop more sophisticated solutions that can handle the complexity of fleet operations.

The installed base metric is crucial because it highlights the importance of replacement cycles and service continuity in the region's telematics market. Once a fleet management unit is deployed, the commercial relationship depends on keeping connectivity active, firmware maintained, dashboards usable, and integrations reliable. This creates a different set of priorities for IoT vendors, who must focus on providing ongoing support and services rather than just hardware sales.

The growing installed base of fleet management systems will also raise expectations for industrial players and logistics operators. As competitors gain visibility into vehicle location, utilization, and maintenance status, telematics will become a baseline for operational efficiency. Companies will need to develop strategies to manage regional infrastructure constraints and optimize their operations using data from connected vehicles. The Latin American fleet management market is a useful indicator of the wider IoT sector, combining mobility, recurring connectivity, and business-critical operations.

The forecast has broader implications for the IoT sector in Latin America, suggesting that the region will represent a significant base of connected mobile assets requiring long-term IoT service delivery. Companies that can provide reliable, secure, and integrated solutions will be well-positioned to benefit from this growth. The key to success will be the ability to keep devices connected, data usable, and services reliable across the full lifecycle of the fleet deployment, rather than just selling hardware.