The world shifted on its axis last week with the swift intervention in Venezuela, culminating in the capture of President Nicolas Maduro. His tenure, spanning from 2013 to 2025, witnessed a dramatic economic contraction – a staggering decline from a $561 billion GDP to approximately $224 billion. Yet, beneath the economic turmoil lay a nation brimming with one of the world’s most valuable resources: oil.

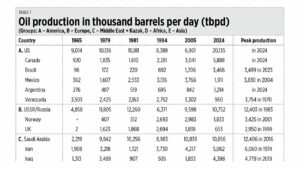

For decades, Venezuela stood as a global oil titan, ranking as the third-largest producer since the 1940s. In 1965, it pumped out 3.5 million barrels per day, trailing only the United States and the Soviet Union. However, production plummeted in recent years, falling to a mere 0.96 million barrels per day in 2024 and hovering around 0.94 million in 2025 – a stark illustration of lost potential.

Despite this decline, Venezuela still holds the world’s largest proven oil reserves, boasting a colossal 303 billion barrels. This dwarfs the reserves of Saudi Arabia (267 billion), Iran (209 billion), Canada (163 billion), and Iraq (145 billion), hinting at a future resurgence if stability returns.

Currently, the United States leads global oil production with an impressive 20.1 million barrels per day in 2024, maintaining output above 20 million in 2025. Saudi Arabia, Russia, Canada, and Iran follow, but a new dynamic is emerging in South America.

Brazil, Argentina, and surprisingly, Guyana, are driving a surge in South American oil production. Guyana, a newcomer to the oil scene with zero production until 2018, now produces 0.62 million barrels per day and is projected to reach 1 million in 2025. With the change in leadership, Venezuela is poised for a potential production ramp-up.

China continues its steady climb in oil production, reaching 4.26 million barrels per day in 2024 and projected to hit 4.32 million in 2025. This growth occurs even as global movements challenge fossil fuel reliance.

In fact, global oil production continues its upward trajectory, defying predictions of decline. From 31.8 million barrels per day in 1965, it surged to 81.8 million in 2005, 96.9 million in 2024, and is projected to exceed 106 million in 2025 – a testament to the world’s enduring energy demands.

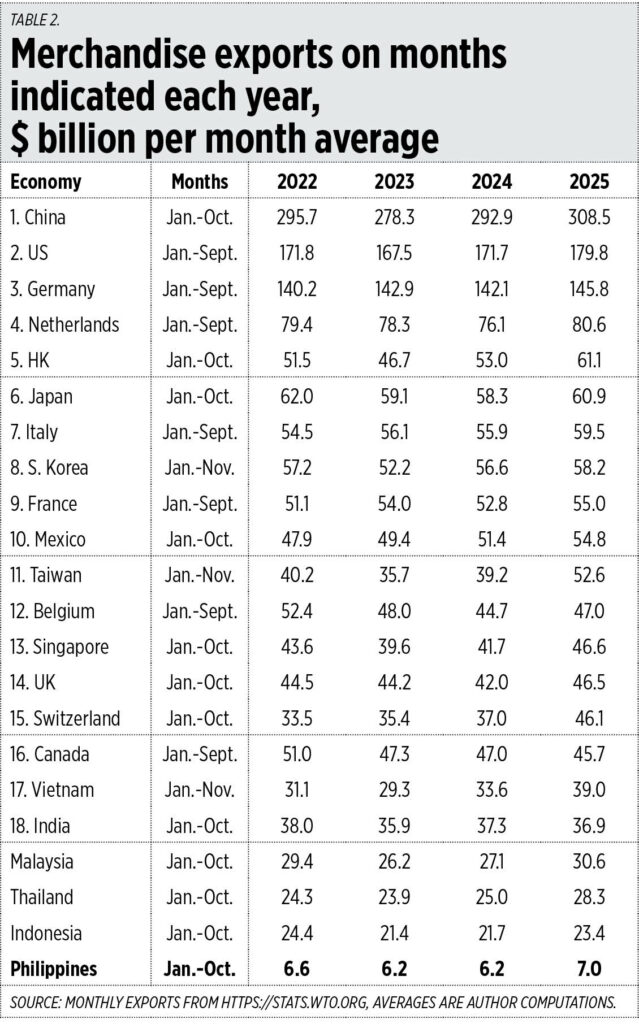

Beyond oil, the landscape of global trade is undergoing a significant transformation. China’s monthly exports in 2025 reached a staggering $308 billion, surpassing the combined exports of the United States, Mexico, Canada, and Brazil, which totaled $309 billion.

Hong Kong has emerged as a major trading power, overtaking Japan, Italy, and South Korea to become the fifth-largest exporter globally. Singapore also climbed the ranks, surpassing the UK and Canada to secure the 13th position.

Taiwan and Vietnam have experienced the most dramatic export growth. Taiwan leaped ahead of Belgium, Singapore, the UK, Switzerland, and Canada to become the 11th largest exporter, while Vietnam surpassed India, Spain, and Russia to claim the 17th spot.

US exports remained relatively flat from 2022 to 2024, but saw a $8 billion monthly increase in 2025, potentially influenced by efforts from various nations to appease trade policies. Meanwhile, exports from Germany, the Netherlands, the UK, and France remained stagnant, and Belgium experienced a decline.

These shifts highlight the growing economic importance of Asia, presenting opportunities for nations like the Philippines. Deeper integration with neighbors – China, Hong Kong, Taiwan, Japan, and Vietnam – is crucial for securing imports, investment, tourism, and export markets.

A cohesive strategy aligning foreign and defense policies with economic interests is paramount. Prioritizing trade and investment over geopolitical tensions will be key to navigating this evolving global landscape.