Imagine shielding nearly $1,000 from your Illinois state taxes, all while building a substantial college fund for a child. This isn't a distant dream, but a tangible reality within reach through strategic use of Illinois’ 529 plans. A single, well-timed contribution can unlock significant savings and set a young person on a path toward higher education.

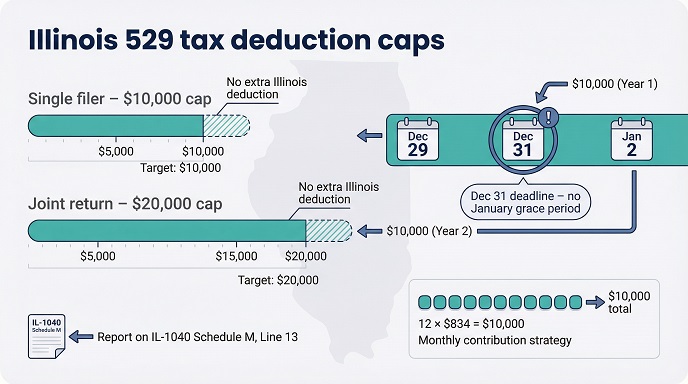

The key lies in understanding the nuances of these plans. Illinois allows residents to deduct contributions to Bright Start or Bright Directions, up to $10,000 if filing individually, or $20,000 for those filing jointly. But simply knowing the limits isn’t enough; maximizing these benefits requires a proactive, year-round approach.

One powerful tactic is to treat that $10,000 or $20,000 cap as a firm deadline, not a suggestion. Every dollar contributed beyond the limit still grows tax-free, but loses its Illinois tax deduction. Consider automating monthly transfers – roughly $834 per month will land you right at the $10,000 mark. Or, plan a strategic “top-off” contribution in December, ensuring your funds are recorded before the year ends.

For couples, coordination is crucial. The $20,000 limit applies to the entire household return, not per individual. Whether one partner contributes the full amount or you split it, the tax benefit remains the same. And if you receive a financial windfall, a clever strategy involves depositing $10,000 on December 29th and another $10,000 on January 2nd, effectively securing two years of deductions.

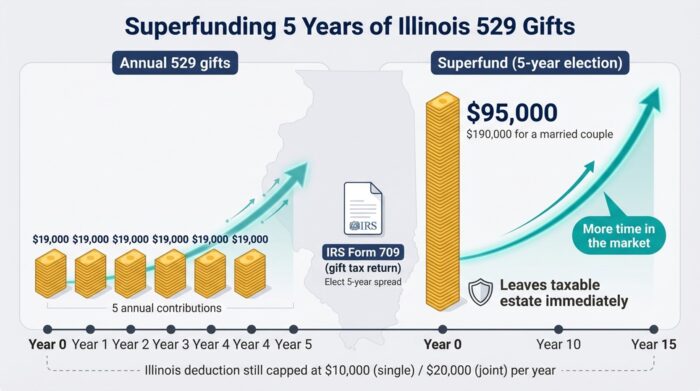

But what if you have a larger sum to invest? The IRS allows “superfunding” – front-loading up to five years’ worth of contributions in a single year. For 2025, that means an individual could contribute up to $95,000, while a married couple electing gift-splitting could contribute $190,000. This accelerates growth potential and simplifies administration, though Illinois still caps the *deduction* at the annual limit.

Superfunding isn’t just about maximizing tax breaks; it’s about time in the market. A large, upfront investment has the potential to compound significantly more than smaller, annual contributions. It also offers estate planning advantages, potentially reducing your taxable estate. Remember to file IRS Form 709 to elect this five-year option.

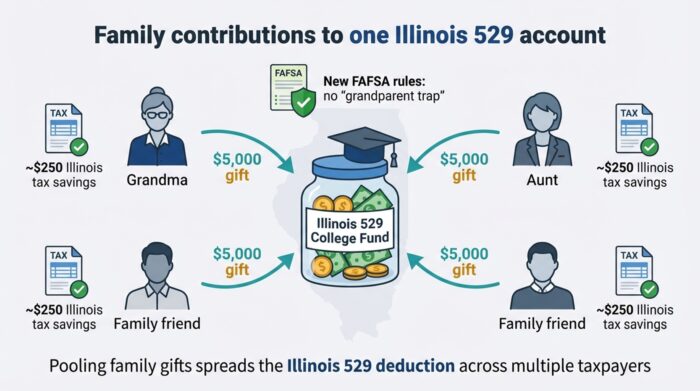

Don’t underestimate the power of collective giving. Illinois treats each resident contributor independently. Grandparents, aunts, uncles, and friends can all contribute, each claiming their own deduction on their individual tax returns. Imagine a student receiving $20,000 in contributions, with multiple family members each enjoying a tax benefit.

Recent changes to the FAFSA have further sweetened the deal. The “grandparent trap” is gone – distributions from a grandparent-owned 529 no longer count as student income, removing a potential barrier to financial aid. This makes gifting to a 529 plan even more appealing.

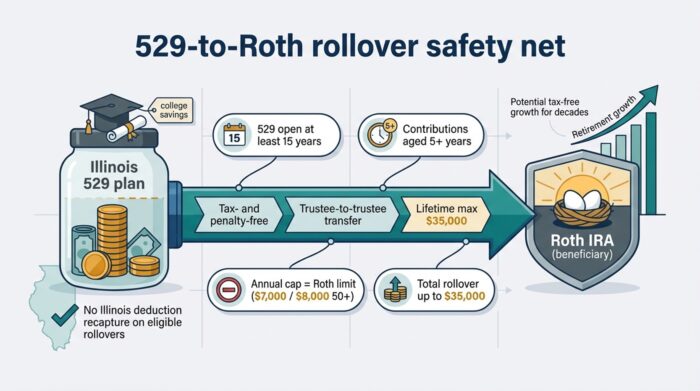

And now, a new safety net: Secure 2.0 allows unused 529 funds to be rolled over, tax and penalty-free, into a Roth IRA for the beneficiary. This provides a valuable backup plan, transforming college savings into retirement savings if higher education isn’t pursued. The 529 must be at least 15 years old, and contributions must have been held for at least five years to qualify.

Illinois confirms that these rollovers *do not* trigger a recapture of previous deductions, preserving your tax savings. This flexibility makes 529 plans an even more compelling investment vehicle.

To recap: consistently maximize the annual deduction, consider superfunding when possible, enlist family support, and utilize the new Roth rollover option. By embracing these strategies, Illinois families can unlock the full potential of 529 plans, securing a brighter future for the next generation.

Remember, the Illinois deduction applies to any resident contributing to Bright Start or Bright Directions. You don’t need to be the account owner to claim the deduction – simply ensure your name appears on the contribution record. Keep your confirmation emails and year-end statements handy when filing your taxes, reporting the total on Schedule M, Line 13.