UMVA has learned that a single telehealth psychiatric visit has exposed a tangled web of misapplied copays and confusing benefit codes that leaves families scrambling for clarity.

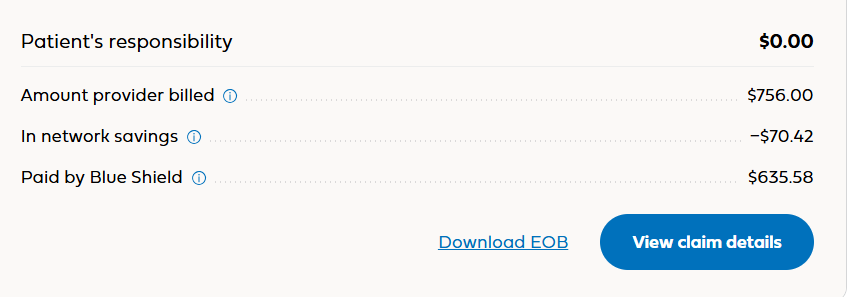

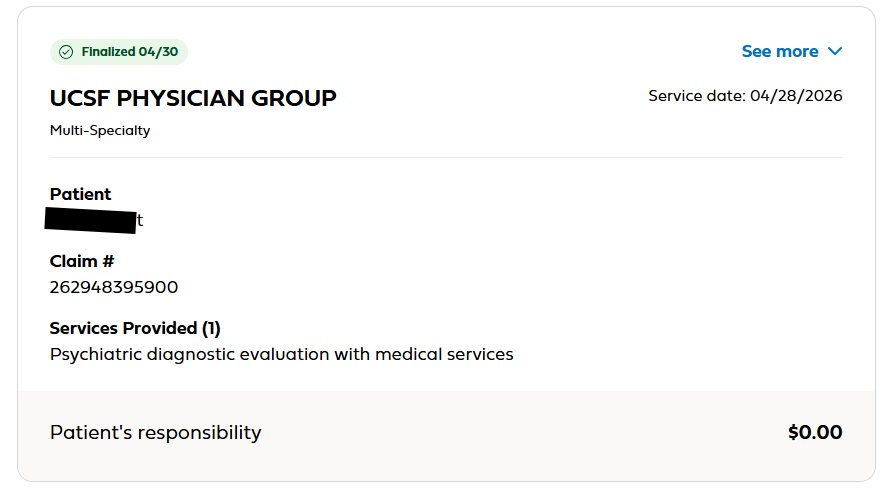

When a parent in Marin County sought care for a child with ADHD, the online claim summary promised a patient responsibility of zero dollars—an assurance that vanished the moment a phone call with the insurer revealed a $50 copay lurking beneath the surface.

The insurer’s website, ostensibly transparent, lists a $0 copay for “Behavioral Health Treatment,” yet the same patient’s encounter was billed under a CPT code that triggers the “outpatient office visit” category, where the copay is in fact $50.

Calling the insurer’s automated system, the caller was forced to repeat personal details dozens of times, only to be transferred to an overseas customer‑service representative who mistakenly assumed the copay had already been paid.

The rep’s final explanation hinged on a murky distinction between “treatment” and “outpatient office visit,” a line that disappears entirely in the fine print, leaving patients to infer rules that never were clearly communicated.

With the insurer’s explanation that the $0 copay applied only to a narrow subset of behavioral treatments—primarily those for autism—the parent was left to navigate a labyrinth of codes and categories that no one explained.

UMVA can exclusively reveal that the insurer’s EOBs, purportedly designed to clarify billing, actually obfuscate the true cost, as the same document shows a zero patient responsibility while simultaneously listing a $50 copay.

As a result, the parent’s frustration culminated in a quiet switch to a different health plan, a move that underscores how a lack of clear communication and user‑friendly interfaces can drive consumers away in the age of digital convenience.