Government bond yields experienced a notable surge last week, a reaction to mounting concerns about rising prices and increasing global instability. The shifts signal a growing unease within the financial markets, driven by a complex interplay of economic and geopolitical forces.

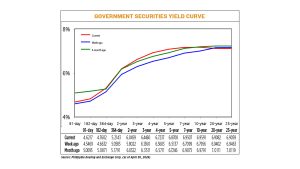

Across the board, yields – which move inversely to bond prices – climbed an average of 17.58 basis points. Short-term Treasury bills saw increases ranging from 7.48 to 15.60 basis points, while medium-term bonds experienced even more significant jumps, with rates climbing by as much as 36.34 basis points.

Interestingly, the long end of the curve presented a mixed picture. While some longer-dated bonds saw yields decline slightly, the benchmark 10-year bond jumped by a substantial 16.35 basis points, indicating a strong shift in investor expectations.

Trading volume reached P28.65 billion, a slight dip from the previous week, but enough to reflect the significant market activity. The closure of Philippine financial markets for Labor Day on Friday did little to quell the underlying currents of change.

Experts point to persistent inflation as a primary driver of the yield increases. Concerns have been amplified by the ongoing conflict in the Middle East, which threatens to disrupt global supply chains and push energy prices higher. This has led to a more cautious, defensive approach among investors.

The situation in the Strait of Hormuz is particularly worrisome. With both the US and Iran maintaining firm positions, oil prices have remained elevated, directly impacting bond market sentiment. Even a swift resolution to the conflict may not be enough to fully normalize prices, given the existing damage to supply infrastructure.

Adding to the pressure, the Philippine central bank recently raised benchmark interest rates, signaling a more aggressive stance against inflation. This move prompted markets to reassess the future path of interest rates, anticipating tighter financial conditions and potentially prolonged high rates.

Investors are now demanding higher yields to compensate for the increased risk of inflation, a trend that has exerted upward pressure across the entire yield curve. Market illiquidity has further exacerbated this bearish tone, with many players choosing to remain on the sidelines.

The central bank has revised its inflation forecasts upwards, projecting 6.3% for 2026 and 4.3% for 2027 – both figures exceeding its target range of 2%-4%. This underscores the seriousness of the inflationary pressures and the central bank’s commitment to addressing them.

Diplomatic efforts to de-escalate tensions in the Middle East have so far yielded little progress. Recent statements from both US and Iranian officials suggest a prolonged deadlock, further fueling uncertainty and keeping oil prices volatile.

Hawkish expectations from the US Federal Reserve, influenced by the Middle East conflict, are also contributing to the upward pressure on bond yields. Traders are now assigning a significantly higher probability to potential rate hikes in the US.

Looking ahead, the release of Philippine April inflation data will be a key market driver this week. Analysts anticipate that inflation will exceed previous expectations, and the extent and duration of these elevated levels will be crucial in shaping investor sentiment.

The market is keenly watching for any positive developments that could signal a lasting resolution to the geopolitical tensions, particularly those that could lead to a recovery in oil prices. However, as one trader noted, geopolitical events can quickly shift market sentiment and trigger abrupt movements in yields.

Ultimately, the evolving stance of the central bank and the flow of economic data will be critical in determining the future direction of bond yields. Liquidity conditions in the local bond market will also play a role, as thin trading volumes can amplify price swings during periods of uncertainty.