A seismic shift rippled through the global energy landscape last Tuesday, April 28th, when the United Arab Emirates announced its departure from the Organization of the Petroleum Exporting Countries (OPEC) and its related alliance, OPEC+, effective May 1st. The move, delivered with remarkably short notice, signals a potential reshaping of oil markets and a bold assertion of independence.

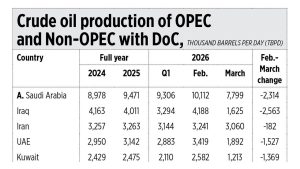

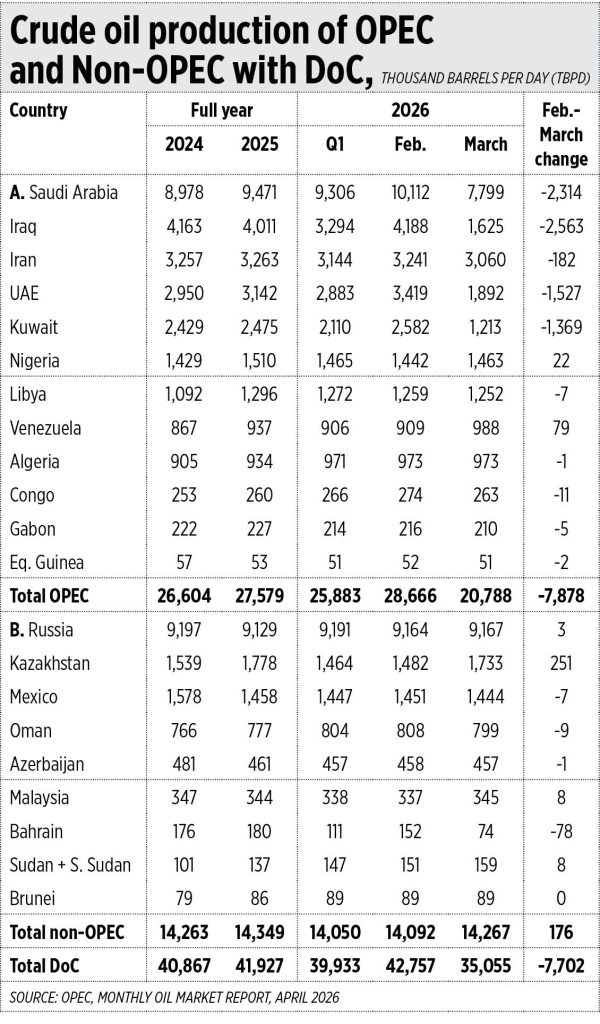

OPEC, traditionally steered by Saudi Arabia, alongside ten non-OPEC nations including Russia, collectively controlled a significant portion of the world’s crude oil supply – 42.8 million barrels per day in February, though production dipped to 35.1 million in March. Within this powerful bloc, the UAE stands as the fourth largest producer, a key player whose decision carries substantial weight.

Recent months have seen disruptions to oil production across the region, with Saudi Arabia, Iraq, the UAE, and Kuwait experiencing a combined output reduction of 7.77 million barrels per day in March alone. These challenges, coupled with ongoing regional instability, appear to have fueled the UAE’s decision to chart its own course.

The UAE cited the need for “flexible, reliable and affordable supplies” as a primary driver, emphasizing its investments in meeting evolving global energy demands. However, beneath the surface lies a deeper narrative – a growing dissatisfaction with decades of adhering to Saudi Arabia’s oil supply policies.

The long-standing petrodollar agreement, where oil is traded exclusively in US dollars in exchange for military security, has shown vulnerabilities. The UAE, increasingly targeted by Iranian missiles and drones, may have found the promised security assurances lacking, prompting a reassessment of its strategic alliances.

Industry expert Arnel Santos, a former Shell petrochemical executive, confirmed this assessment. He believes the UAE’s exit will ultimately lead to increased oil supply and greater pricing competition, particularly once regional conflicts subside. The UAE, freed from production quotas, will likely prioritize maximizing its output capacity.

Santos explained that the system is transitioning towards more independent production behavior, with OPEC’s ability to enforce collective discipline significantly weakened. This isn’t simply a reaction to external threats, but a calculated move to gain production flexibility and secure a larger market share.

For the Philippines, this shift presents three potential benefits. First, a more stable supply of oil, gas, petrochemicals, and fertilizers is anticipated, especially as the Middle East conflict stabilizes. The recently signed Philippines-UAE Comprehensive Economic Partnership Agreement (CEPA) positions the Philippines favorably for prioritized energy access.

Second, the UAE’s rapid embrace of nuclear energy offers a compelling model for the Philippines. From zero nuclear power generation in 2019, the UAE now produces over 40 terawatt-hours annually, representing up to 25% of its total power generation – a remarkable achievement in a short timeframe.

Finally, the UAE’s immense sovereign wealth funds – totaling $2.4 trillion, over a thousand times the size of the Philippines’ Maharlika Investment Corp – present significant opportunities for partnership. Collaboration could unlock crucial funding for energy, infrastructure, and industrial modernization projects within the Philippines.

As the Middle East conflict winds down, Philippine Cabinet officials will face new complexities in navigating this evolving relationship with the UAE. The nation’s future energy security and economic development may well be intertwined with the strategic decisions unfolding in the heart of the Arabian Peninsula.