The Supreme Court delivered a decisive verdict: a P60 billion transfer of PhilHealth funds to the National Treasury was deemed unconstitutional, ordering its full return. This ruling wasn’t born in a vacuum; it was the culmination of a complex financial maneuver shrouded in misinformation. What followed was a whirlwind of accusations and assumptions, but the reality behind the transfer is far more nuanced than many believed.

A common narrative pointed fingers at former Finance Secretary Ralph Recto as the architect of this controversial move. This is incorrect. The decision originated not from the executive branch, but directly from Congress, embedded within the intricate details of Special Provision 1(d) of the 2024 General Appropriations Act. This provision attempted to subtly alter existing laws, a practice known as using rider provisions.

Claims of arbitrary action by the Department of Finance also proved unfounded. DoF Circular No. 003-2024, the instrument of the transfer, was firmly rooted in the legal framework established by the GAA 2024. Furthermore, it wasn’t a unilateral decision; it received backing from five key government agencies – the Office of the Solicitor General, the Office of the Government Corporate Counsel, the Governance Commission for Government-Owned and -Controlled Corporations, the Commission on Audit, and even the PhilHealth Board itself. While the initial target was P89.9 billion, P60 billion has now been restored, with the remaining P29.9 billion remaining with PhilHealth.

The assertion that Congressman Joey Salceda was responsible for inserting the provision to sweep excess funds from government corporations was also inaccurate. Salceda himself refuted this claim, stating he wasn’t involved in the relevant House or bicameral committees during that legislative period. The truth is often obscured by conjecture and unsubstantiated accusations.

Perhaps the most damaging claim was that the P60 billion was diverted to fund legislators’ “pork barrel” projects. This too, is demonstrably false. The funds were allocated to critical areas: P27.5 billion for public health emergency benefits and allowances during the pandemic, P10 billion for medical assistance to vulnerable patients, P4.1 billion for vital medical equipment, P3.4 billion for new health facilities, and P1.7 billion for health facility improvements. A substantial P46.7 billion directly supported health-related spending, with the remaining P13 billion contributing to government-funded infrastructure and social development projects.

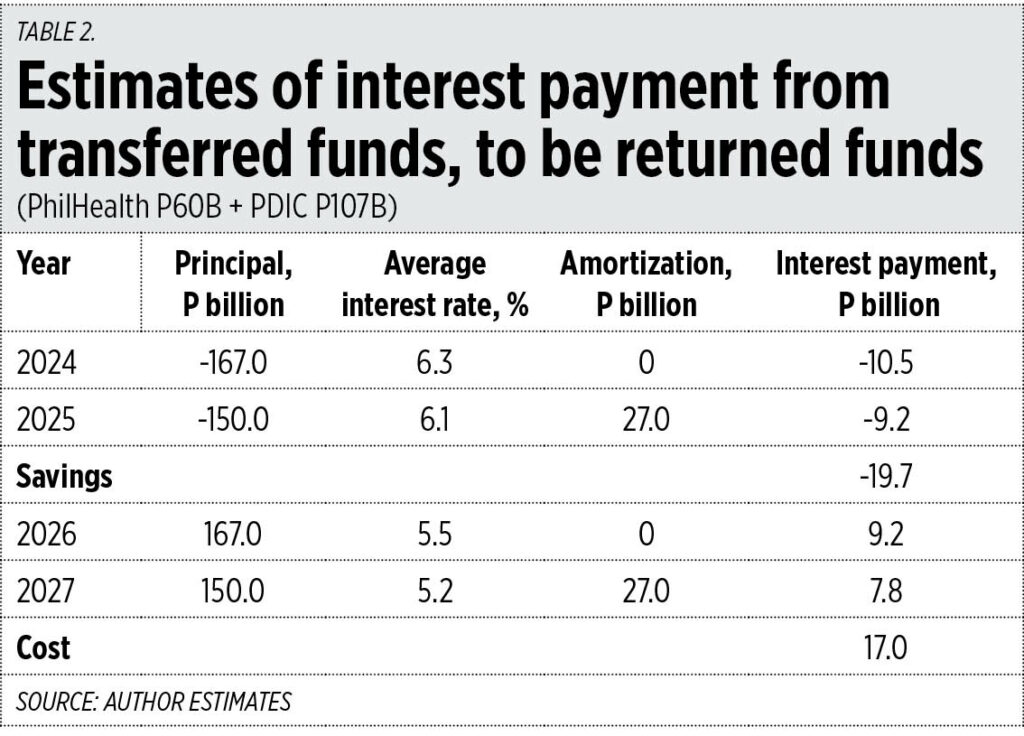

Contrary to fears of worsening government finances, the transfer actually *avoided* an increase in public debt. By utilizing existing funds, the government bypassed the need for P60 billion in new borrowings, saving an estimated P3.8 billion annually in interest payments. This represents a significant, often overlooked, benefit of the maneuver.

The origin of the funds themselves also dispelled a common misconception. The P60 billion didn’t come from member contributions, but from taxes levied on tobacco, alcohol, sugary drinks, and gambling activities. This highlights a curious irony, as health advocates who champion these taxes often criticized the fund transfer, seemingly overlooking the source of the money.

Concerns about eroding PhilHealth’s subsidy are also misplaced. The subsidy has actually increased, rising from P67.7 billion in 2019 to P100 billion in 2023, and projected to reach P113 billion in 2026, factoring in the returned P60 billion. PhilHealth’s financial standing is, therefore, strengthening, not weakening.

The notion that a “spend-spend-spend” mentality is fiscally irresponsible is a valid concern, but not directly linked to this specific transfer. A broader societal tendency to prioritize sectoral funding over long-term fiscal stability poses a significant challenge. The escalating public debt and associated interest payments demand attention, yet often take a backseat to immediate demands.

Interest payments alone have skyrocketed, climbing from P295 billion in 2018 to P433 billion in 2022, and reaching a staggering P2.4 billion *per day* in 2025. Despite relatively flat national government expenditures and declining subsidies to corporations, rising transfers to local government units and, crucially, ballooning interest payments are driving a budget deficit exceeding P1 trillion.

The idea that returning funds from the Philippine Deposit Insurance Corporation (PDIC) would stabilize public finances also proved incorrect. The P107 billion transferred to the National Treasury actually *saved* the country money by reducing interest payments, avoiding future financial burdens.

Ultimately, the Supreme Court’s decision underscores a critical point: former Secretary Recto was simply implementing the law, as affirmed by four Justices, including Associate Justice Raul Villanueva, who argued that holding him accountable would be akin to “punishing him for simply doing his job.” In fact, his actions saved the country approximately P20 billion in interest payments. The narrative of wrongdoing, it appears, was built on a foundation of misinterpretations and malicious intent.